Market Brief CAD and JPY Supported Following Attack On Oil Production Facility

{kind=link}

- The US officially blamed Iran for this weekend’s attack on the world’s largest oil facility in Saudi Arabia. Trump tweeted that the US was “locked and loaded”, hinting at a potential response over the attack. Oil prices are back below $60 after gapping higher over 12% today.

- China data came in weaker than expected, with urban investments slowing to 5.5% YoY (weakest in 12 months), industrial output falling to 4.4% (weakest since 2002) and retail sales felling to 7.5% versus 7.9% expected. This is all despite further stimulus earlier this year, which will no doubt spur further calls for yet more stimulus.

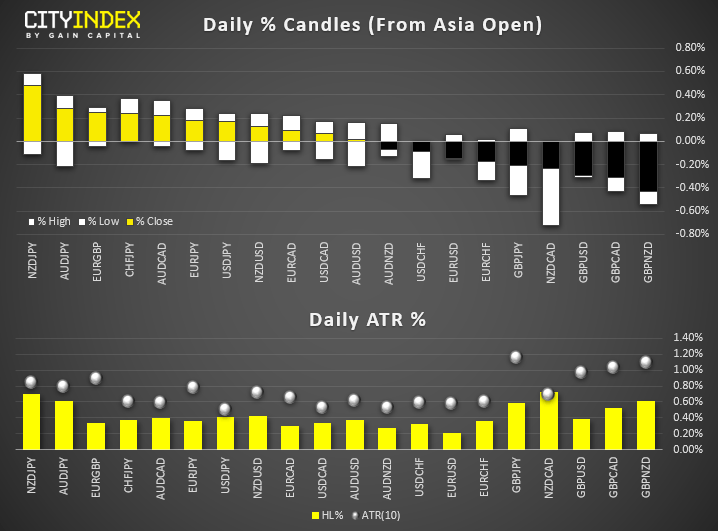

- CAD is the strongest major, supported by higher oil prices. JPY is the second strongest major from safe-haven flows, seeing USD/JPY gap to a 2-day low and trade back beneath April’s bearish trendline. GBP is today’s weakest major, although remains near Friday’s highs.

- Despite the weekend drones’ attack on Saud Arabia’s oil production that has sent the WTI crude oil futures to spike close to 10% in today’s Asian session, the overall performance seen so far on Asian stock markets have appeared to be quite muted despite an increase in Middle East’s geopolitical risk. U.S. has put the blame on Iran for the attacks and President Trump tweeted with a “lock and loaded” response that hinted a potential retaliation towards Iran.

- Also, industrial production from China for Aug came in below expectation at 4.4% y/y versus consensus of 5.2% y/y. It has continued to decline from Jul data of 4.8% y/y that has led to a 3rd consecutive month of slower growth from the negative effects of the on-going U.S-China trade tension.

- The worst performer so far as at today’s Asia mid-session is Hong Kong’s Hang Seng Index where it has dropped by -1.00%. The weaker sentiment seen in the Hang Seng Index versus its Asian peers is likely due to localised factors. Firstly, the negative spill-over effect from another bout of violent weekend clashes between police and anti-government protestors where mass protests have entered the 15th week. Secondly, London Stock Exchange (LSE) has rejected Hong Kong Stock Exchange (HKSE) US$39 billion takeover bid. Despite HKSE’s refusal to give up on its bid for LSE, shares of HKSE has dropped by -2.7% to hit a 4-week low of 234.40 as seen today.

- S&P 500 E-mini has gapped down in today’s Asian open session and traded lower to print a current intraday low of 2983; a drop of -0.86%. Right now, as at today’s Asian mid-session, it has recouped some of its earlier losses to trade at 2990; a current intraday drop of -0.61%.

Up Next:

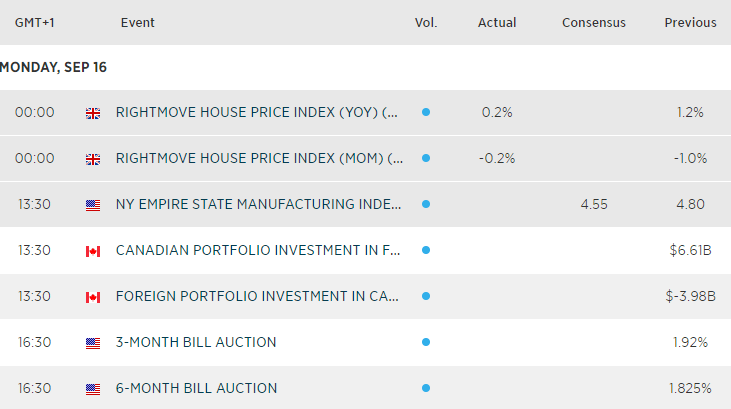

- Data is light for the US session (and non-existent for the European). And with trade tensions taking a back seat, it’s any update or knock-on effect from the weekends oil plant attack which could be a key driver for markets. Markets to watch: WTI, Brent, CAD, NOK, RUB

{kind=link}

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.This report is intended for general circulation only. It should not be construed as a recommendation, or an offer (or solicitation of an offer) to buy or sell any financial products. The information provided does not take into account your specific investment objectives, financial situation or particular needs. Before you act on any recommendation that may be contained in this report, independent advice ought to be sought from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs.

StoneX Financial Pte. Ltd., may distribute reports produced by its respective foreign entities or affiliates within the StoneX group of companies or third parties pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed to a person in Singapore who is not an accredited investor, expert investor or an institutional investor (as defined in the Securities Futures Act), StoneX Financial Pte. Ltd. accepts legal responsibility to such persons for the contents of the report only to the extent required by law. Singapore recipients should contact StoneX Financial Pte. Ltd. at 6826 9988 for matters arising from, or in connection with the report.

In the case of all other recipients of this report, to the extent permitted by applicable laws and regulations neither StoneX Financial Pte. Ltd. nor its associated companies will be responsible or liable for any loss or damage incurred arising out of, or in connection with, any use of the information contained in this report and all such liability is hereby expressly disclaimed. No representation or warranty is made, express or implied, that the content of this report is complete or accurate.

StoneX Financial Pte. Ltd. is not under any obligation to update this report.

Trading CFDs and FX on margin carries a high level of risk that may not be suitable for some investors. Consider your investment objectives, level of experience, financial resources, risk appetite and other relevant circumstances carefully. The possibility exists that you could lose some or all of your investments, including your initial deposits. If in doubt, please seek independent expert advice. Visit www.cityindex.com/en-sg/terms-and-policies for the complete Risk Disclosure Statement.

ALL TRADING INVOLVES RISKS. LOSSES CAN EXCEED DEPOSITS.

City Index is a trading name of StoneX Financial Pte. Ltd. (“SFP”) for the offering of dealing services in Contracts for Differences (“CFD”). SFP holds a Capital Markets Services Licence issued by the Monetary Authority of Singapore for Dealing in Exchange-Traded Derivatives Contracts, Over-the-Counter Derivatives Contracts, and Spot Foreign Exchange Contracts for the Purposes of Leveraged Foreign Exchange Trading. SFP is also both Derivatives Trading and Clearing member of the Singapore Exchange (“SGX”). SFP is a wholly-owned subsidiary of StoneX Group Inc.

The information provided herein is intended for general circulation. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should take into account your specific investment objectives, financial situation or particular needs before making a commitment to invest, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit. No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk.

The information does not represent an offer of, or solicitation for, a transaction in any investment product. Any views and opinions expressed may be changed without an update. To understand the risks and costs involved, please visit the section captioned “Important Information” and the “Risk Disclosure Statement”.

The information herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

StoneX Financial Pte. Ltd. 1 Raffles Place, #18-61, One Raffles Place Tower 2, Singapore 048616. Tel: 6309 1000. Co. Reg. No.: 201130598R.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

© City Index 2024