Market Brief AUD Bulls Contained by Risk Off and AU GDP

View our guide on how to interpret the FX Dashboard

{kind=link}

FX Brief:

- Australia’s GDP missed expectations at 0.4% QoQ vs 0.5% expected. It didn’t take long for twitter to mock RBA’s ‘gentle turning point’ in the economy. Earlier, service PMI expanded but at a slower pace of 53.7 vs 54.2 prior. Ultimately, it still appears likely RBA will cut in Q1 and possibly as early in February (1st meeting of the year).

- US House voted to impose Chinese sanctions over human rights abuses over the Uighur Muslim Minority. Another factor to consider for how ‘well’ phase one trade talks are going.

- British pound remains supported after yesterday’s polls show conservatives widening their lead.

- China’s service PMI expanded at its fastest pace in 7 months at 53.5, up from 51.1 prior. Hong Kong’s PMI slumps to 38.5.

Price Action:

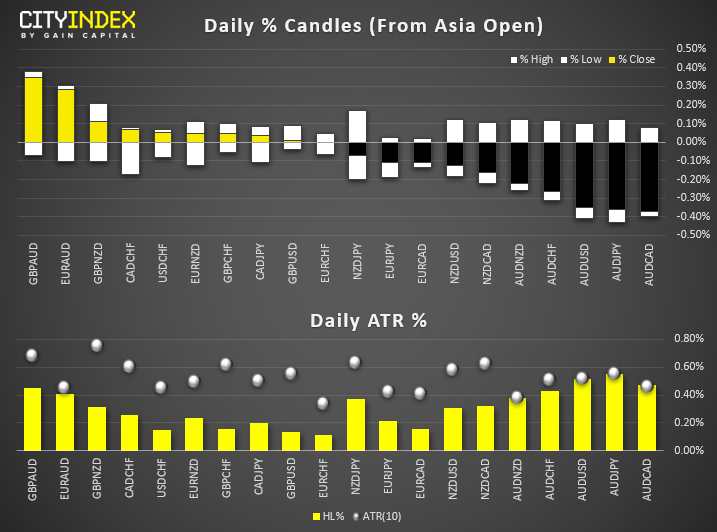

- CHF and JPY were the strongest currencies as trade war worries deepened. No daily ranges are yet to exceed their daily ATR’s, although AUD/JPY, AUD/USD and EUR/AUD came the closest after AUD fell following weaker than expected GDP figures.

- With DXY balancing precariously on 97.68 support, traders are now waiting for to see if a corrective rebound or bearish breakdown will now follow.

- EUR/USD has paused at 1.1093 resistance as expected, printing a rikshaw man doji (indecision candle) below resistance.

- GBP/USD closed just shy of 1.3000 overnight and is teasing traders with a bullish breakout of this key level. An inverted head and shoulders pattern could be in the making (a continuation pattern during an uptrend) which projects and approximate target around 1.3250 is successful.

- NZD/USD’s rally stalled perfectly near its upper channel yesterday, leaving the door open to a period of consolidation (further out we anticipate new highs for NZD crosses).

- USD/CNH remains just off its 30-day high. It’s essentially a barometer of how well trade talks are going. Given they’re not going well, the yuan is weaker – which is something else which will likely irk President Trump.

Equity Brief:

- Risk off continues to rage in key Asian stock markets where trade worries have resurfaced again after U.S. President Trump has resumed his “Tariff Man” alter ego. Trump has commented that he has no urgency for a trade deal with China that has dashed the hopes of the much hyped “final throes” Phase One deal signed off before the 15 Dec deadline kicks in for another round of U.S. tariffs on Chinese products.

- Media has reported that according to sources from U.S. trade department that the U.S. administration is set to impose the 15% tariffs on US$160 billion worth of Chinese products on 15 Dec if U.S and China cannot agree to a Phase One trade deal.

- On the geopolitical front, more tension is on the rise between U.S. and China that can derail the prospect of a trade deal. The U.S. House has passed the Xinjiang Bill that sought to enact sanctions on China over human rights abuses and prohibit the export of certain U.S. technologies products that can be used in state-sponsored suppression.

- Australia’s ASX 200 is the worst performer for the 2nd consecutive session with a loss of -1.58%. The current losses in the past 3 days have now wiped out the entire monthly gain for Nov. Energy and Industrial stocks led the bears where both sectors have tumbled by around 2% so far.

- Losses in China stock market has been muted with the China A50 that has only shed -0.15% supported by a resilient China’s service industry despite the on-going trade tensions. The Caixin/Market Services PMI for Nov rose to 53.5 from 51.10 in Oct, a 7-moth high and the fastest pact of expansion since Apr 2019. It also surpassed consensus forecast that is set at 52.7.

Price Acton (derived from CFD indices):

- Japan 225: Minor downtrend from 02 Dec 2019 swing high remains intact with further potential downside to test the key medium-term support at 22700 (former swing high areas of 08 Nov/03 Dec 2018 & 21 Nov 2019 swing low). Key short-term resistance stands at 23200 (minor descending trendline from 02 Dec 2019 high & former 03 Dec 2019 swing low).

- Hong Kong 50: Broke below the lower boundary of the ascending range configuration in place since 15 Aug 2019 low now turns pull-back resistance at 26300 with risk of further downside to test the next near-term support at 25660/500 (28 Sep/10 Oct 2019 swing low areas).

- Australia 200: Tumbled and hit the 6630 range support in place since 21 Oct 2019 with extreme oversold readings seen in short-term momentum oscillators which suggests an overextended decline. Watch the 6655 minor resistance (former 21 Nov 2019 minor swing low) & a break above 6655 sees a minor mean reversion rebound towards 6740/6780 (50%/61.8% retracement of the on-going decline from 29 Nov 2019 high).

- US SP 500: Broke below the 3110 (the gapped up from 22/25 Nov 2019 & the lower boundary of the ascending channel from 03 Oct 2019 low). Now at risk of further downside towards the next near-term support at 3045 (lower boundary of minor descending channel from 02 Dec 2019 high & 0.618 Fibonacci expansion of the current down move from 02 Dec high to 03 Dec low projected from today’s Asian session high of 3096). Key short-term resistance stands at 3113.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.This report is intended for general circulation only. It should not be construed as a recommendation, or an offer (or solicitation of an offer) to buy or sell any financial products. The information provided does not take into account your specific investment objectives, financial situation or particular needs. Before you act on any recommendation that may be contained in this report, independent advice ought to be sought from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs.

StoneX Financial Pte. Ltd., may distribute reports produced by its respective foreign entities or affiliates within the StoneX group of companies or third parties pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed to a person in Singapore who is not an accredited investor, expert investor or an institutional investor (as defined in the Securities Futures Act), StoneX Financial Pte. Ltd. accepts legal responsibility to such persons for the contents of the report only to the extent required by law. Singapore recipients should contact StoneX Financial Pte. Ltd. at 6826 9988 for matters arising from, or in connection with the report.

In the case of all other recipients of this report, to the extent permitted by applicable laws and regulations neither StoneX Financial Pte. Ltd. nor its associated companies will be responsible or liable for any loss or damage incurred arising out of, or in connection with, any use of the information contained in this report and all such liability is hereby expressly disclaimed. No representation or warranty is made, express or implied, that the content of this report is complete or accurate.

StoneX Financial Pte. Ltd. is not under any obligation to update this report.

Trading CFDs and FX on margin carries a high level of risk that may not be suitable for some investors. Consider your investment objectives, level of experience, financial resources, risk appetite and other relevant circumstances carefully. The possibility exists that you could lose some or all of your investments, including your initial deposits. If in doubt, please seek independent expert advice. Visit www.cityindex.com/en-sg/terms-and-policies for the complete Risk Disclosure Statement.

ALL TRADING INVOLVES RISKS. LOSSES CAN EXCEED DEPOSITS.

City Index is a trading name of StoneX Financial Pte. Ltd. (“SFP”) for the offering of dealing services in Contracts for Differences (“CFD”). SFP holds a Capital Markets Services Licence issued by the Monetary Authority of Singapore for Dealing in Exchange-Traded Derivatives Contracts, Over-the-Counter Derivatives Contracts, and Spot Foreign Exchange Contracts for the Purposes of Leveraged Foreign Exchange Trading. SFP is also both Derivatives Trading and Clearing member of the Singapore Exchange (“SGX”). SFP is a wholly-owned subsidiary of StoneX Group Inc.

The information provided herein is intended for general circulation. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should take into account your specific investment objectives, financial situation or particular needs before making a commitment to invest, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit. No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk.

The information does not represent an offer of, or solicitation for, a transaction in any investment product. Any views and opinions expressed may be changed without an update. To understand the risks and costs involved, please visit the section captioned “Important Information” and the “Risk Disclosure Statement”.

The information herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

StoneX Financial Pte. Ltd. 1 Raffles Place, #18-61, One Raffles Place Tower 2, Singapore 048616. Tel: 6309 1000. Co. Reg. No.: 201130598R.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

© City Index 2024