Burberry outlook survives Hong Kong

The unpredictable HK backdrop keeps guidance static despite a promising first half

Burberry shares are justifiably pricing back in profit expectations that were trimmed on worries over Hong Kong unrest and China growth. Britain’s leading purveyor of finery comfortably matched first-half 2020 sales expectations whilst pacing revenue and earnings forecasts, as sales accelerated in recent months.

Key H1/Q2 results

- Comparable H1 retail sales +4%, in line with estimates

- Comparable Q2 retail sales, +5% vs. +4.6% est.

- H1 revenue: £1.281bn vs. £1.26bn est.

- Comparable H1 operating profit: £186m vs. £172.3m est.

(Note H1 op. profit was £202m under recently adopted IFRS accounting standard)

Solid results partly reflect delivery on the promise of debut collections by chief designer Riccardo Tisci. Any doubt that a strong initial reception would hold into later quarters ought to have been softened given double-digit growth based in new products. Robust figures and firm demand overall demonstrate that anticipated disruption from unrest in Hong Kong was contained though the extent of its impact was still sobering. Burberry shares initially surged 9% on Thursday, their best one day move in four months. But the revelation in a post-earnings presentation that retail sales fell 38% in Hong Kong trimmed the rise to as little as 3.5%. With further “significant negative impact” expected in over Q3, the risks to full-year forecasts—which Burberry has maintained—can’t be ignored.

What’s positive about the HK situation is that the group doesn’t foresee further impairment charges there, after booking a £14m H1 hit, without details. More broadly, other key regions gave no fresh cause for alarm. And whilst currency impact and advantages from the new accounting format gave a non-operational lift, resilient demand still underpinned underlying profits. As well, the efficiency programme is on track for annual £135m savings targeted by 2022 with £110m in costs also intact.

The final impression is that the firm played its latest challenging hand adroitly, whilst the trump card of exclusive and rarefied designs is working out better than planned. True, old inventory continues to weigh on margins. And the verdict on the strength of new high-margin items (e.g. handbags) needs to be withheld till availability of Tisci’s collections reaches 80% of the ‘mainline’ offer from 70% in Q2. The buzzy Tencent alliance is just as difficult to quantify, though nice to have. It will neither hinder nor help Burberry with key challenges in the months ahead.

The positive though volatile stock reaction reflects improved stability but also continued uncertainty that the luxury group can escape its minnow status and also-ran valuation relative to European rivals anytime soon.

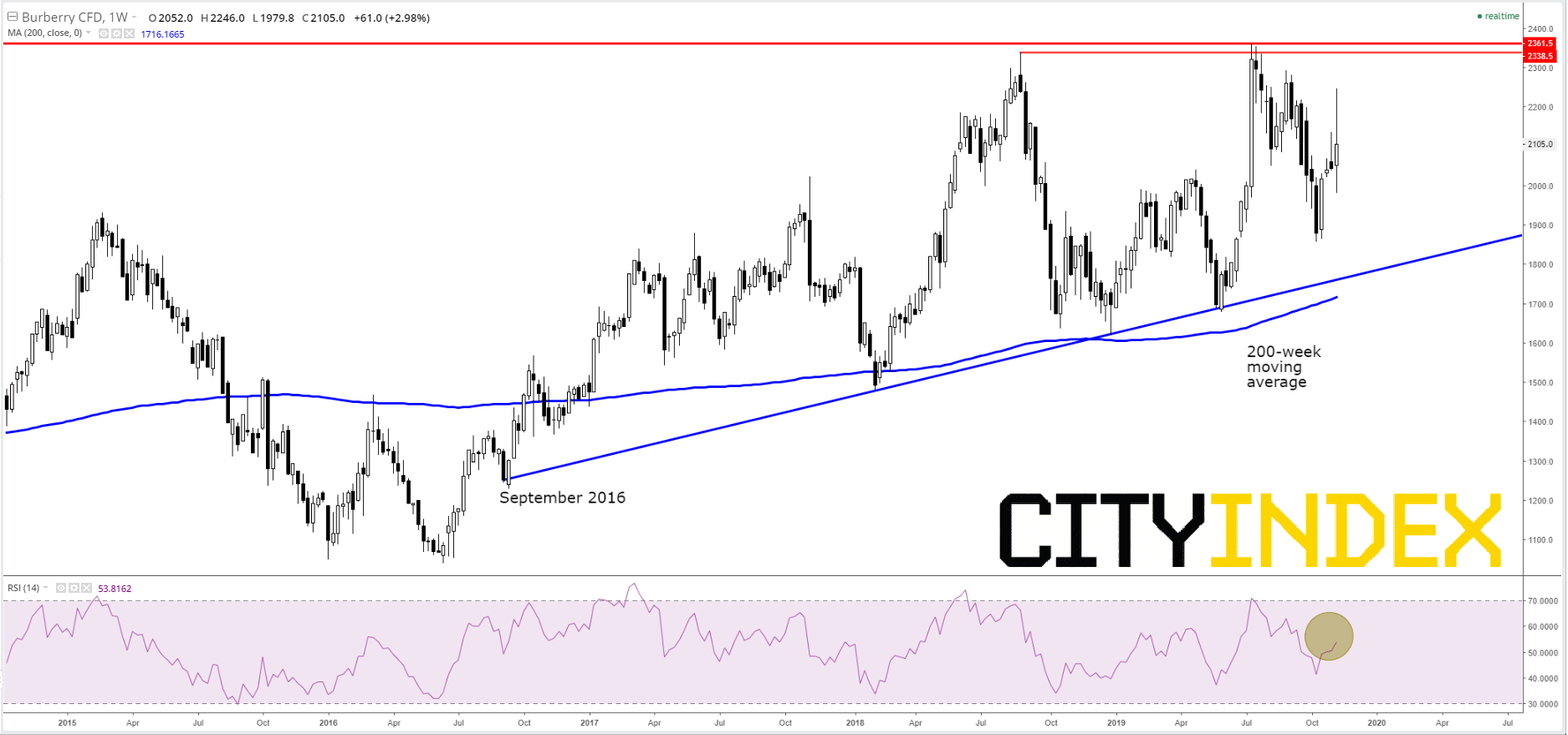

Chart points

Uptrend intact, the upside case continues to hinge on the difference between the cleanest trend of recent years, stemming from early September 2016, and peak resistance around 2340p-2360p. Investors must decide when or whether momentum will suffice on the share’s next attempt at the above highs, to surpass them. Sellers will have the opposite judgement to make. With the 200-week average now adding support to the dominant rising line, whilst RSI momentum also rallies with plenty of room to run, BRBY at least looks set to drift up towards another attempt at those highs as the year winds up.

Burberry Group Plc. CFD – Weekly

{kind=link}

Source: City Index

This report is intended for general circulation only. It should not be construed as a recommendation, or an offer (or solicitation of an offer) to buy or sell any financial products. The information provided does not take into account your specific investment objectives, financial situation or particular needs. Before you act on any recommendation that may be contained in this report, independent advice ought to be sought from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs.

StoneX Financial Pte. Ltd., may distribute reports produced by its respective foreign entities or affiliates within the StoneX group of companies or third parties pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed to a person in Singapore who is not an accredited investor, expert investor or an institutional investor (as defined in the Securities Futures Act), StoneX Financial Pte. Ltd. accepts legal responsibility to such persons for the contents of the report only to the extent required by law. Singapore recipients should contact StoneX Financial Pte. Ltd. at 6826 9988 for matters arising from, or in connection with the report.

In the case of all other recipients of this report, to the extent permitted by applicable laws and regulations neither StoneX Financial Pte. Ltd. nor its associated companies will be responsible or liable for any loss or damage incurred arising out of, or in connection with, any use of the information contained in this report and all such liability is hereby expressly disclaimed. No representation or warranty is made, express or implied, that the content of this report is complete or accurate.

StoneX Financial Pte. Ltd. is not under any obligation to update this report.

Trading CFDs and FX on margin carries a high level of risk that may not be suitable for some investors. Consider your investment objectives, level of experience, financial resources, risk appetite and other relevant circumstances carefully. The possibility exists that you could lose some or all of your investments, including your initial deposits. If in doubt, please seek independent expert advice. Visit www.cityindex.com/en-sg/terms-and-policies for the complete Risk Disclosure Statement.

ALL TRADING INVOLVES RISKS. LOSSES CAN EXCEED DEPOSITS.

City Index is a trading name of StoneX Financial Pte. Ltd. (“SFP”) for the offering of dealing services in Contracts for Differences (“CFD”). SFP holds a Capital Markets Services Licence issued by the Monetary Authority of Singapore for Dealing in Exchange-Traded Derivatives Contracts, Over-the-Counter Derivatives Contracts, and Spot Foreign Exchange Contracts for the Purposes of Leveraged Foreign Exchange Trading. SFP is also both Derivatives Trading and Clearing member of the Singapore Exchange (“SGX”). SFP is a wholly-owned subsidiary of StoneX Group Inc.

The information provided herein is intended for general circulation. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should take into account your specific investment objectives, financial situation or particular needs before making a commitment to invest, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit. No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk.

The information does not represent an offer of, or solicitation for, a transaction in any investment product. Any views and opinions expressed may be changed without an update. To understand the risks and costs involved, please visit the section captioned “Important Information” and the “Risk Disclosure Statement”.

The information herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

StoneX Financial Pte. Ltd. 1 Raffles Place, #18-61, One Raffles Place Tower 2, Singapore 048616. Tel: 6309 1000. Co. Reg. No.: 201130598R.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

© City Index 2024