Big banks fight Fed cuts to grow earnings

Goldman and Morgan Stanley earnings are forecast to come out worst in the third quarter whilst Citigroup’s could soar

A quarter with two Federal Reserve interest rate cuts has proved to be a challenging one for the big U.S. banks as they kick off the earnings season this week. Even so, a deep, across-the-board earnings decline is not widely expected. Instead, consensus forecasts point two a couple of laggards weighing down the average for the group that includes ‘megabanks’ JPMorgan, Bank of America, Citigroup and Wells Fargo; and the somewhat smaller, by assets, Goldman Sachs and Morgan Stanley.

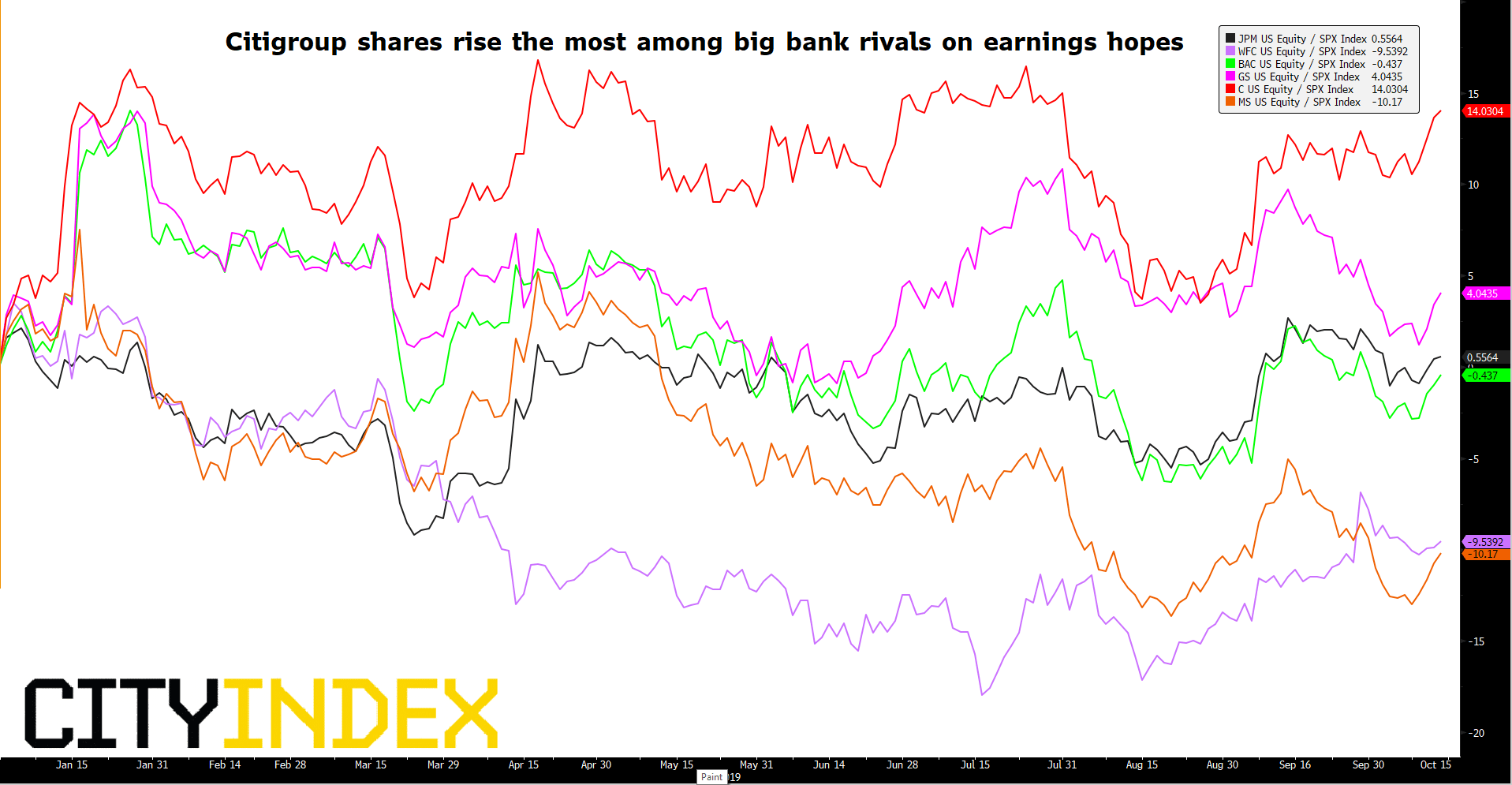

Data provider Refinitiv says investors are expecting the dominant U.S. banks to post their first year-on-year quarterly decline in three years. Earnings per share is set for a 1.2% fall versus the third quarter of 2018 though revenue could grow by 0.9% . Still, Goldman is expected to drag overall performance most, with an EPS that’s seen tumbling 21%, whilst consensus forecasts point to a 6% drop for Morgan Stanley. Most of the other major U.S. lenders could report modestly improving income, though Citigroup could outpace all if a 13% estimate of its third quarter earnings growth proves accurate. Such expectations help account for Citi’s share price outperformance of peers so far this year.

Normalised: Big U.S. banks relative to S&P 500 – year to date [14/10/2019 20:09:40]

{kind=link}

Source: City Index

Investors are particularly watching out for the impact of falling interest rates on net interest margins. With key Treasury yield curves inverted for much of the year, banks’ typical ‘borrowing short and lending long’ protocol hasn’t worked as well as it usually does. For one thing, costlier short-term rates and cheaper long-term rates can drive a cart and horses through short-term interbank lending whilst crushing long-term loans rates on mortgages.

The silver lining is that lower Fed rates have underpinned the mortgage market as borrowers are enticed in and refinancing, which accounts for most U.S. mortgage applications, trends higher. A strong consumer, amid multi-year lows in unemployment and a still relatively solid economy should underpin consumer credit businesses. That will be a boon particularly for chief mortgage lenders, Bank of America and Wells Fargo, though a 50% rise in applications on last year, according to Mortgage Bankers Association data out last week, also likely reflects continued aggressive expansion of JPMorgan’s consumer and business lending franchise.

At the same time, investors will be vigilant for any sign that slowing though still strong U.S. economic conditions may have begun to crimp loan growth. August volatility spikes ought to have boosted banks’ trading revenues annually, though quarter-to-quarter performance may be more challenged. And the worst quarter for around two years in M&A and a troubled turn for IPOs is expected to put single-digit percentage pressure on the average investment banking revenue result.

The main points to watch for and the timing of each large U.S. bank’s earnings are below.

Wells Fargo & Co Q3 2019 earnings – 15th October, before U.S. market open

The problem U.S. bank is still not allowed to grow its asset base due to a Federal Reserve restriction that was a punishment for WFC’s infamous fake accounts scandal. The key news in recent weeks has been that the bank has appointed a new CEO after a multi-month search. Buybacks and dividend raises are expected to continue though declining net-interest revenue and elevated costs linked to regulatory costs will likely haunt Wells for many more years to come. Underlying EPS is seen up 1.5%, since Q3 2018, to $1.175 with revenue growth of 1.4% to $21.156bn.

JPMorgan Chase & Co. Q3 2019 earnings – 15th October, before U.S. market open

Rising digital spending—JPM is among the biggest tech spenders this year—gives it an edge in active mobile accounts. A lower average tax rate and cost discipline should help protect margins from the worst effects of Fed cuts. Provisions for loan losses are another watch point as JPM stays ahead in credit card and other loans. Q3 EPS is seen rising 5% on the same quarter a year ago to $2.45. Revenues are forecast up 2.4% at $24.48bn.

Citigroup Inc. Q3 2019 earnings - 15th April, before U.S. market open

Citi will rely on a steady improvement in efficiency to offset the effect of one more probable Fed rate cut in 2019—looking at market-based indicators—than the bank reportedly planned for. A shortfall relative to recent guidance may need to be addressed when the group reports. Q3 EPS is expected to be $1.95, a rise of almost 13% year-to-year, with revenues inching 0.75% higher at $18.52bn.

Goldman Sachs Group Inc. Q3 2019 earnings, 15th October, before U.S. market open

Goldman reclaimed (some of) its mantle as the leading bank for trading clients in the prior quarter, making GS markets performance in Q3 easily the biggest point to watch. With Deutsche Bank’s significant retreat from markets businesses in the quarter, Goldman’s path has probably been smoother. On a quarterly basis, markets revenues may not surpass Q2, but they’re expected to rise year-on-year. Adjusted EPS is seen at $4.95, a 21% drop following a tough quarter to beat last year. Revenues are expected down 3.3% at $8.36bn.

Bank of America Corp. Q3 2019 earnings, 16th October, 11.45 BST

BofA’s capital return has improved to well above the level representing a pay-out of all attributable earnings to shareholders. That’s a turnaround for BofA investors given that the group lagged rivals on dividend and other pay-outs for years. Progress on deposit and asset growth will now need to be shown to maintain that momentum. Expect EPS at $0.65, up 2.6% on the year, with revenues dipping 1% to $22.76bn.

Morgan Stanley. Q3 2019 earnings, 17th October, before U.S. market open

The smallest bank by market cap and assets is forecast to report a 6.2% EPS fall to $1.116, with revenue of $9.57bn equating to a 3% slide. MS’s pivot to a bigger emphasis on wealth management relative to peers is expected to keep a shine on that segment. However it has continued to perform worst in the Fed’s annual stress tests, even with an apparently solid capital position. This helps account for the stock’s 10% drop relative to the S&P 500 so far this year, as investors shy away from perceived risk despite progress on growth.

This report is intended for general circulation only. It should not be construed as a recommendation, or an offer (or solicitation of an offer) to buy or sell any financial products. The information provided does not take into account your specific investment objectives, financial situation or particular needs. Before you act on any recommendation that may be contained in this report, independent advice ought to be sought from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs.

StoneX Financial Pte. Ltd., may distribute reports produced by its respective foreign entities or affiliates within the StoneX group of companies or third parties pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed to a person in Singapore who is not an accredited investor, expert investor or an institutional investor (as defined in the Securities Futures Act), StoneX Financial Pte. Ltd. accepts legal responsibility to such persons for the contents of the report only to the extent required by law. Singapore recipients should contact StoneX Financial Pte. Ltd. at 6826 9988 for matters arising from, or in connection with the report.

In the case of all other recipients of this report, to the extent permitted by applicable laws and regulations neither StoneX Financial Pte. Ltd. nor its associated companies will be responsible or liable for any loss or damage incurred arising out of, or in connection with, any use of the information contained in this report and all such liability is hereby expressly disclaimed. No representation or warranty is made, express or implied, that the content of this report is complete or accurate.

StoneX Financial Pte. Ltd. is not under any obligation to update this report.

Trading CFDs and FX on margin carries a high level of risk that may not be suitable for some investors. Consider your investment objectives, level of experience, financial resources, risk appetite and other relevant circumstances carefully. The possibility exists that you could lose some or all of your investments, including your initial deposits. If in doubt, please seek independent expert advice. Visit www.cityindex.com/en-sg/terms-and-policies for the complete Risk Disclosure Statement.

ALL TRADING INVOLVES RISKS. LOSSES CAN EXCEED DEPOSITS.

City Index is a trading name of StoneX Financial Pte. Ltd. (“SFP”) for the offering of dealing services in Contracts for Differences (“CFD”). SFP holds a Capital Markets Services Licence issued by the Monetary Authority of Singapore for Dealing in Exchange-Traded Derivatives Contracts, Over-the-Counter Derivatives Contracts, and Spot Foreign Exchange Contracts for the Purposes of Leveraged Foreign Exchange Trading. SFP is also both Derivatives Trading and Clearing member of the Singapore Exchange (“SGX”). SFP is a wholly-owned subsidiary of StoneX Group Inc.

The information provided herein is intended for general circulation. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should take into account your specific investment objectives, financial situation or particular needs before making a commitment to invest, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit. No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk.

The information does not represent an offer of, or solicitation for, a transaction in any investment product. Any views and opinions expressed may be changed without an update. To understand the risks and costs involved, please visit the section captioned “Important Information” and the “Risk Disclosure Statement”.

The information herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

StoneX Financial Pte. Ltd. 1 Raffles Place, #18-61, One Raffles Place Tower 2, Singapore 048616. Tel: 6309 1000. Co. Reg. No.: 201130598R.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

© City Index 2024