Though massive beatings could become less frequent from here

The latest and most spectacular collapse of shares in Micro Focus, the FTSE 100 group whose ‘legacy’ software strategy continues to come unstuck, is a dump of as much as 34%. That’s the £4bn group’s deepest one-day collapse since an almost 50% crash on 19th March 2018. Then, like now, it was downgraded guidance that spooked investors. Holders have become so hypersensitive to possible understatement of revenue downside, they precipitate the very value destruction they’re trying to avoid in the first place. Its another unfortunate consequence of MCRO’s $8.8bn acquisition of Hewlett Packard Enterprise assets that has turned out to be little short of disastrous

There are fair reasons to see Wednesday’s slump as even more of an over-reaction. The stock remained 30% lower into afternoon trading, despite only a fairly marginal downgrade of already dire expectations. The group reduced guidance of its expected full-year revenue decline to a range of -6% to -8% in constant currency terms, from -4% to -6% before. The cut looks just as symbolic as it might be material. That’s assuming the group even has sufficient visibility to predict a two-percentage point sales growth reduction, at the midpoint, relative to previous forecast. Either way, it’s hard to square the toasting of £1bn-plus in market value over a change that could be worth about $69m, given 2019 revenues seen around $343bn. (MCRO reports results in dollars).

There’s no question MCRO’s outlook remains deeply unattractive, but the case for ‘rock bottom’ is growing more cogent:

- The new CEO had already began to jettison weak assets after launching a review process some months, before MCRO’s latest downgrade

- After Thursday’s drama, Stephen Murdoch is doubling down: "Following the recent disappointing trading performance, we have determined that it is appropriate to accelerate the undertaking of a strategic review.” No further details are offered for now

- His approach has already resulted in the disposal of SUSE (a Linux pioneer) for $2.54bn. Further ‘bolt-off’ disposals are probable as MCRO unwinds years of bolt-on buys with questionable rationales

- Asset sales subsequent to Elliott Management’s stake build are almost certainly not coincidental

- At multiple of 5 times 2020’s estimated $860m free cash flow, MCRO ought to tempt buyers, though the concept of a wholesale buy-out would hold more water further down the line

- The medium-term focus remains on continued disposals of least-accretive units

- That won’t dial down the stock price pain any time soon. Therefore—upticks aside—further downside into Q4 is likely

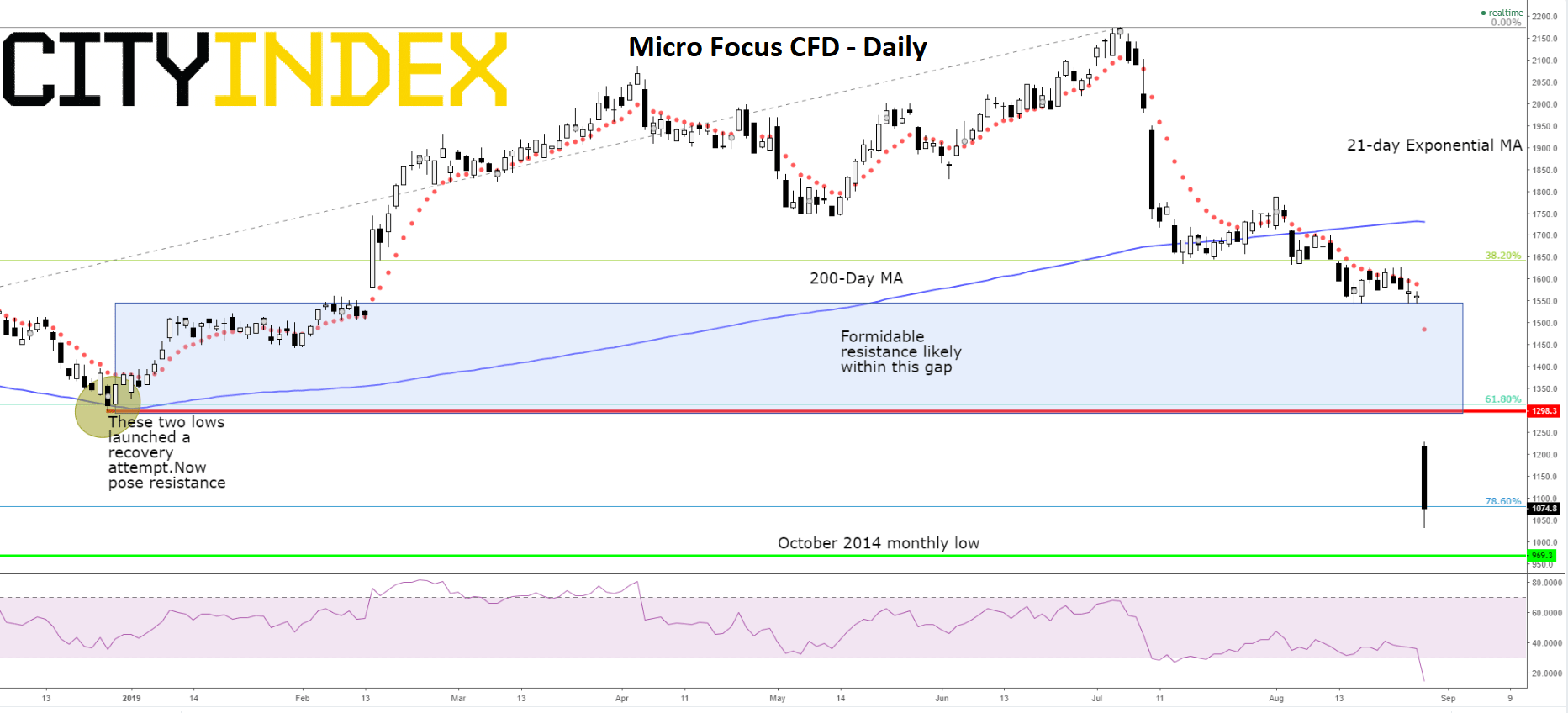

Chart thoughts

- Technically speaking, MCRO is nowhere near ‘rock-bottom’. It has held off from March 2018’s 771p low by some margin, also avoiding long-term support initially codified by October 2014’s 969p low

- The 78.6% retracement of its April 2018-July 2019 top has assisted the stock on Thursday

- Based on a Relative Strength Index (RSI) that hasn’t been more oversold in 16 months, MCRO has a greater chance of a melt-up than of melting down further

- Counter-arguments include that the huge gap opened Thursday is reinforced by a 61.8% retracement interval

- That is pennies away from a double-tagged kick-back low from late December ‘18/early-January ’19

- The underside of the determined buying seen then should be an obdurate resistance to go higher from here, unless there’s significant fundamental improvement

Micro Focus CFD – Daily

Source: City Index

Latest market news

Today 08:15 AM

Latest Earnings articles

Yesterday 01:15 PM

April 21, 2024 04:00 AM

April 18, 2024 04:46 PM