A last-minute surge of PPI costs damped the quarter but that is the least of the bank’s worries

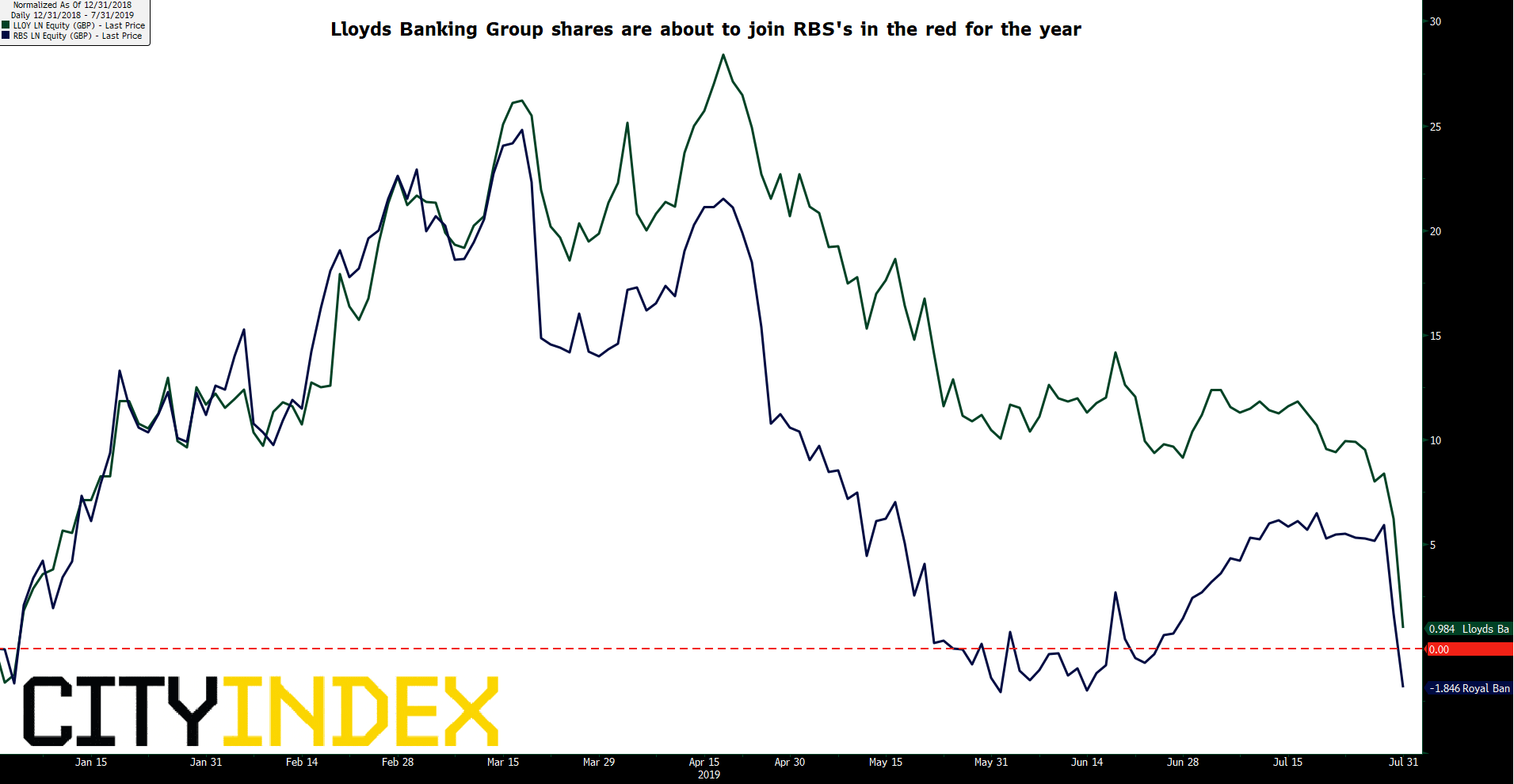

It’s difficult to see how Lloyds Banking Group could have performed more robustly given the specific challenges of the quarter. Looked at this way, perhaps the accelerated downturn of its shares on Wednesday is not entirely justified. The bigger picture helps explain why investor confidence continues to ebb. At last check, the shares had trimmed 4% more off a 2019 advance that stood almost 30% higher at mid-April. Now, they’re barely up 2% for the year and looking likely to turn negative.

The bank points to a fresh charge of £500m linked to payment protection insurance (PPI) as primarily responsible for missed second-quarter expectations.

The key misses

- Statutory pre-tax profit: £1.294bn vs. £1.76bn estimate

- 2Q net interest income: £3.06bn vs. £3.16bn consensus

- 2Q underlying profit: £2.03bn, below company-compiled £2.05bn consensus

- 2Q net interest margin: 2.89% vs. 2.94% estimate

Bloomberg consensus unless specified

But beyond the headline misses, the outlook weighs more. Hopes were pinned on the possibility that rising efficiency and lower regulatory and business capital needs, could enable swifter dividends rises and share buybacks. The interim dividend rose 5% to 1.12 pence; in line with expectations, which is exactly the point.

“Below the line charges”, including the last-minute wave of PPI costs have scuppered those hopes for now. Lloyds’ boast of sufficient capital for growth, regulatory requirements, uncertainty and a ‘management buffer’, have come a cropper as it now expects 2019 leeway to be at the lower end of a 170-200 basis point range. It implies that’s the reason why it’s holding back from a nearer term increase of capital returns. A fairly solid first-half despite misses adds a random variable.

- Total costs fell a more than forecast 5%, operating costs -3%

- Cost: income ratio on course for low 40% levels by end-2020, better than comparable rivals

- The wealth management push is bearing early fruit whilst insurance is stable

“Continued economic uncertainty could impact” the outlook as clarified on Wednesday, the bank says. Despite economic “resilience” it is nodding to Brexit risks for a decision to hang fire on pay-outs, perhaps for even longer than the first quarter of 2020.

More broadly, if the first half was sobering for Lloyds investors, it should be more worrying for RBS holders. They will find out how that bank fared in the first half on Friday. RBS faces a sharper delta from declining economic confidence and is the runner-up in Britain’s mortgage market. The stock was down 3% at time of writing and is slightly weaker for the year than Lloyds’. On the basis of results from its bigger rival, it’s set to continue leading the downside.

Normalised: Lloyds Banking Group, RBS – year-to-date [31/07/2019 13:14:42]

Source: Bloomberg/City Index

Latest market news

Today 08:15 AM

Latest Lloyds articles

April 21, 2024 04:00 AM

February 22, 2023 02:59 PM

February 20, 2023 09:18 AM

July 27, 2022 08:00 AM