Recap Q2 2022

The first half of the year proved to be a perfect storm for the markets. Heading into the start of the year, there was no way we could have foreseen what was coming.

The Russian invasion of Ukraine accelerated the rise in inflation; central bankers started to take inflation seriously, ramping up interest rates, and recession fears emerged.

The past three months were particularly challenging to trade as equities plunged, as did the US safe haven 10-year treasury bond, leaving few places for investors to hide.

The S&P500 saw its worst start to the year since the 1970s and the Nasdaq since 2002 as big tech crashed. The yen tumbled 15.5%, and commodities saw the strongest rally in over 40 years.

So what can we expect going forwards?

Themes in Q3

Heading into Q3, the bearish bias for stocks is expected to stay. US CPI is at 8.6%, and consumer prices are at a record high in Europe. Hence, momentum will likely remain to the downside as the cost of living crisis bites, particularly as central banks aggressively tighten monetary policy, driving recession fears. Markers will continue looking for signs of passed peak inflation. This is expected sooner in the US than in Europe, although even after passing peak inflation, it is expected to be an extended slow return to the central bank’s target levels for CPI.

Central banks

Major central banks across the globe have started (or in the case of the ECB) are about to begin hiking interest rates aggressively. Powell, Lagarde, and Andrew Bailey voiced their commitment to tighten monetary policy to tame inflation, even at the cost of a recession. Across the coming quarter, central bank action will be more focused than ever, as will guidance for the final quarter. In some cases, such as the UK, growth is expected to continue slowing considerably.

China

China’s zero-COVID policy resulted in harsh lockdowns across some of its main cities. It hurt sentiment, saw economic activity slow considerably in China, and disrupted global supply chains. While activity is ramping up again and quarantine for international travelers has been reduced in a positive sign. The reopening of China could help keep commodity prices supported. However, the prospect of further lockdowns remains as long as China sticks with its zero-tolerance policy.

Russian war

The Russian war is rumbling on. Day-to-day attacks and comments regarding the war no longer move the market as they did at the start of the invasion. However, Putin using gas as a political weapon, particularly heading towards the autumn and winter, could keep gas prices and inflation in Europe elevated.

Markets

FX

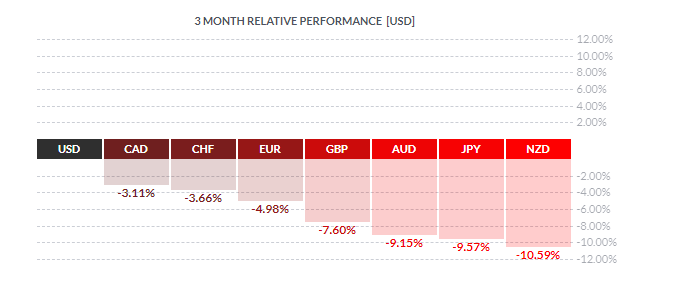

King dollar ruled across the previous quarter as Fed rate hike bets grew. The Federal Reserve is expected to raise rates by 75 basis points in July, followed by a 50 basis point hike in September. Should expectations build around a 75 basis point hike in September, the USD will have already rallied over 5% in Q2 and could continue climbing.

The Fed’s moves highlight central bank divergence with the BoJ, which has boosted USD/JPY to a 24-year high in Q2. Should recession fears rise sharply, the yen could find support from safe-haven flows. Alternatively, investors will be looking for signs that the BoJ could start to turn more hawkish as their policy looks increasingly out of sync with the rest of the world, bosting the yen. However, there haven’t been any signs yet.

The BoE started hiking rates at the end of 2021. However, inflation has risen to 9.1% YoY in May and is expected to continue rising to 11% in the coming months. A combination of Brexit, a tight labor market, and a high reliance on imported energy mean that the UK is experiencing an income shock far worse than its western peers. According to the OECD, growth will also be slowest in the UK compared to other G7 nations. GDP growth contracted in March and April.

The rising risk of recession is clouding the BoE outlook for continuing to hike rates, which has pulled the pound to 1.21 heading into Q3. The GB[P is likely to remain under pressure across Q3 as growth continues to struggle and the market questions the BoE’s ability to hike as much as they hope to.

ECB is yet to start the hiking cycle. A rate hike is expected in July, followed by an outsized hike in September, although this hefty rate hike could occur as the region sits on the brink of recession which could keep the euro depressed. News surrounding the ECB’s anti-fragmentation tool will be closely watched.

Learn more about forex trading hoursIndices

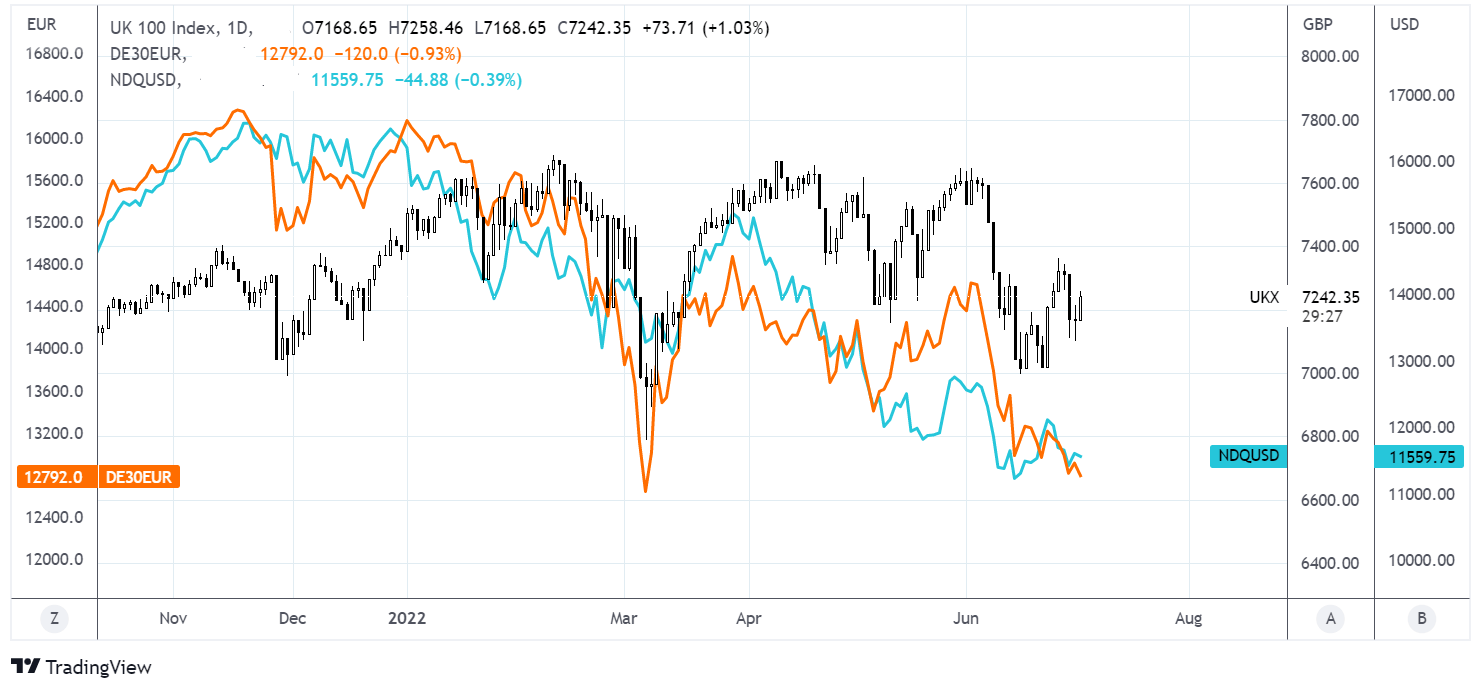

FTSE has been an outperformer compared to its European and US peers, thanks in parts to the weaker pound and surging oil prices, lifting heavyweight oil majors. Looking across the coming quarter, the FTSE has the potential to continue to find support from energy prices which are expected to remain broadly supported.

In the US, the Nasdaq has underperformed, falling 23% across the quarter as high-growth tech stocks fell out of favor as interest rate expectations rose. The bearish momentum could continue through Q3 until peak inflation has passed and as investors continue weighing up the likelihood of a recession in the US.

On a sector level, consumer staples, healthcare, and utilities often outperform in the early stages of a recession.

Commodities

Oil prices have jumped 6% across Q2 and are down 20% from the March high. Tight supply continues to keep oil prices supported. However, concerns over the demand outlook as recession fears rise offset those supply-side fears and could continue to do so. OPEC+

Gold fell almost 7% across the previous quarter as rate hike expectations hit demand for non-yielding USD-denominated gold. With central banks expected to continue hiking rates, Gold is likely to remain under pressure falling meaningfully below $1800.

Latest market news

Today 08:15 AM

Today 05:45 AM

Latest Trade Ideas articles

Today 08:15 AM

Today 05:45 AM