Asian Indices:

- Australia's ASX 200 index rose by 39.6 points (0.55%) and currently trades at 7,217.40

- Japan's Nikkei 225 index has risen by 158.88 points (0.57%) and currently trades at 28,200.36

- Hong Kong's Hang Seng index has fallen by -120.57 points (-0.59%) and currently trades at 20,279.54

- China's A50 Index has risen by 9.52 points (0.07%) and currently trades at 13,246.04

UK and Europe:

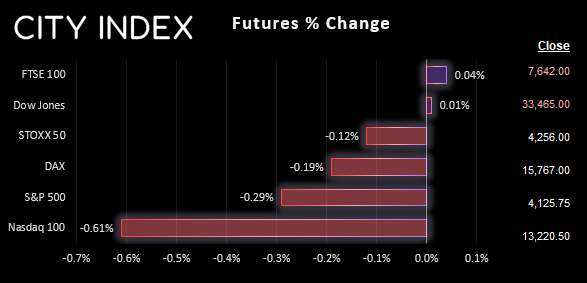

- UK's FTSE 100 futures are currently up 3.5 points (0.05%), the cash market is currently estimated to open at 7,635.24

- Euro STOXX 50 futures are currently down -5 points (-0.12%), the cash market is currently estimated to open at 4,310.05

- Germany's DAX futures are currently down -31 points (-0.2%), the cash market is currently estimated to open at 15,597.84

US Futures:

- DJI futures are currently up 4 points (0.01%)

- S&P 500 futures are currently down -11.75 points (-0.28%)

- Nasdaq 100 futures are currently down -80.75 points (-0.61%)

- Oil gapped aggressively higher at the Asian open and rallied nearly 8%, on news that OPEC+ announced they are cutting oil production by over 1 million barrels per day

- The OPEC move was quickly called “inadvisable” by the US, as it risks a second round of inflation at a time that central authorities have yet to fully deal with the first one

- Gold has fallen around 1% today as investors weigh up the lure of gold as a safe haven asset, versus the potential for higher-for-longer interest rates. Clearly, fears of inflation and higher interest rates has won the argument with gold heading for $1950.

- Given its repeated failed attempts to break above $2000, gold is now vulnerable to a move down to $1900 given the potential for a higher terminal Fed rate that markets are currently pricing in.

- Nasdaq futures are 0.6% lower as tech stocks remain sensitive to higher rates

- The DAX and STOXX are also lower, but to a lesser degree of -0.19% and 0.12% respectively

- China and Hong Kong exchanges were closed due to the Ching Meng Festival between Monday and Wednesday

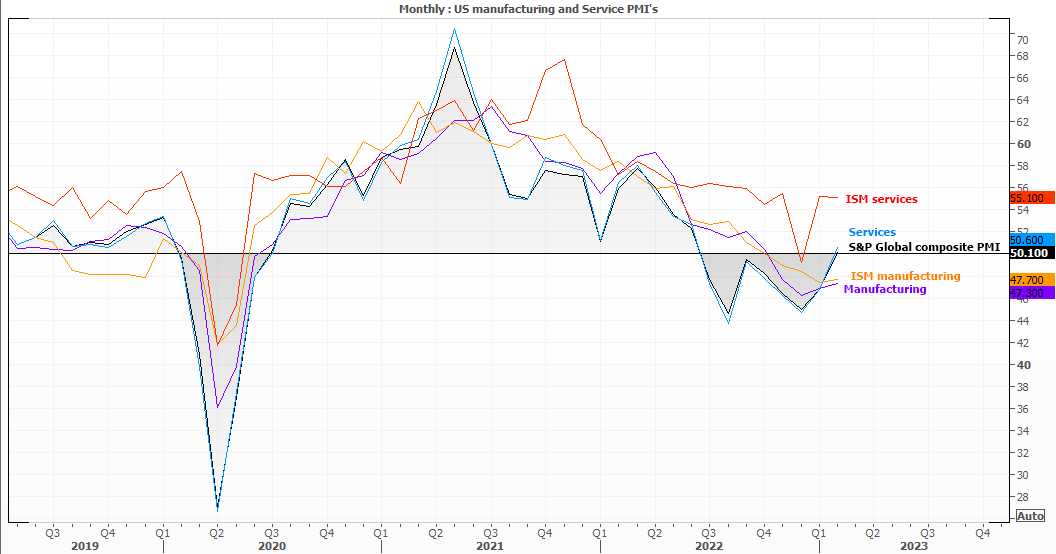

- PMI across Asia was a little lacklustre, which saw China’s manufacturing PMI stall at 50 (neither expand or contract), Japan’s manufacturing PMI contract at 49.7 (below 51 previous and 51.3 prior) and South Korea’s manufacturing PMI contract at a faster rate of 47.6 (48.5 prior)

I think OPEC’s move has killed the argument for Fed rate cuts and plays into the ‘no cuts this year’ message that Jerome Powell has been peddling. It could be argued that OPEC’s move really is more of a lesson for bond traders than it is for the Fed, as the central bank are all too aware that higher oil prices could bring a second wave of inflation and result in a higher terminal rate further out.

With OPEC reminding markets that they will not hesitate to support oil prices, it’s not impossible to envisage oil hitting the $90-$100 range. And that is a major problem for central banks and governments in the fight against inflation.

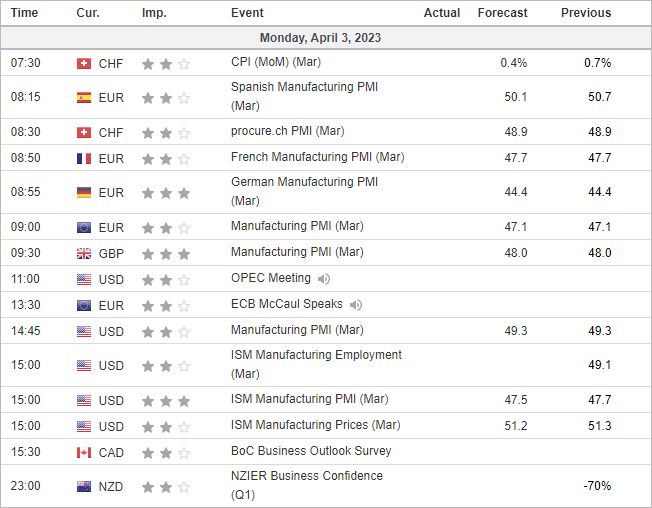

A host of PMI reports are released today

PMI reports provide a forward look at potential growth of a country or region, and today we have flash PMI reports for Europe, UK and the US. If early reports from Asia are anything to go by, we may be in for some softer manufacturing reports or faster rates of contraction. The ‘prices paid’ sub index warrants a look to see if inflation pressures continue to soften, whilst the ‘new orders’ component shows a pipeline of potential out, and can therefor lead the headline figures.

Italy kicks off at 07:45 GMT+1, France and Germany follow at 8:50 and 8:55, the eurozone at 09:00 and the UK at 09:30. Of those mentioned, Italy has the only expansion in February – at the slow rate of 51. Ultimately, we won’t hold our breath for any punchy manufacturing figures today. The ISM report on business is also released at 15:00 for US manufacturing and services.

Swiss CPI also in focus at 07:30

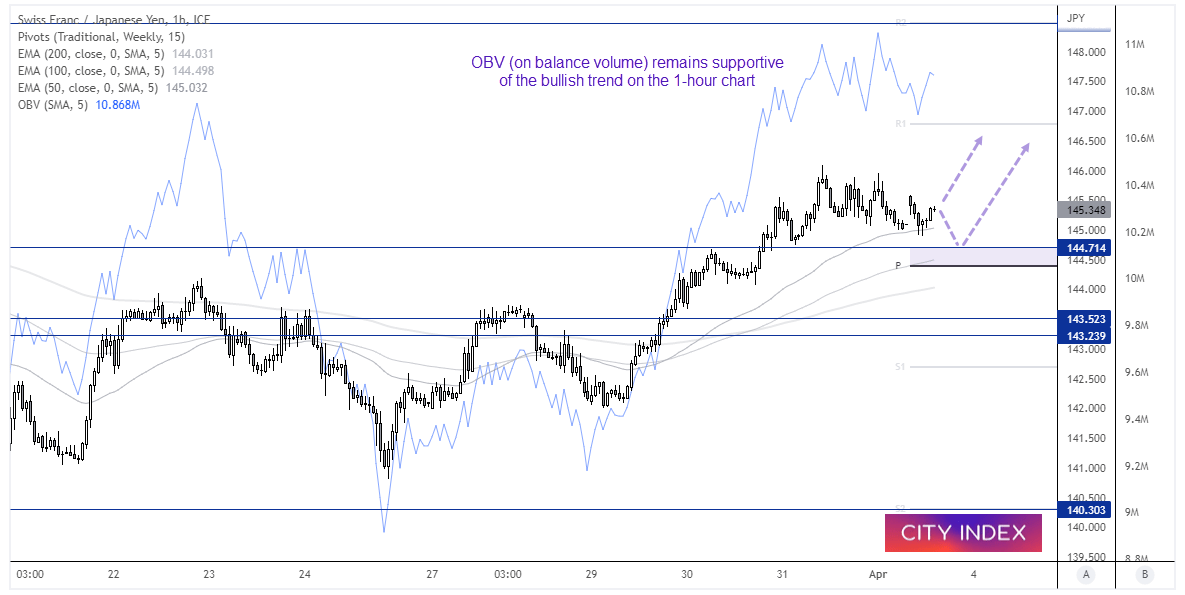

The SNB (Swiss National Bank) delivered a hawkish hike in December, have continued to make hawkish noise since whilst citing high levels of inflation. Therefore, a stronger Swiss inflation report today could cement another SNB hike and further support the Swiss franc. Take note that the yen is currently the weakest major, and a bullish trend has developed on the 1-hour CHF/JPY chart.

Prices are holding above 145 ahead of today’s inflation report, and we’re looking for a bullish breakout from its current consolidation and move up to the weekly R1 pivot around 146.60.

Economic events up next (Times in GMT+1)

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 07:49 AM

Today 04:24 AM

Yesterday 10:48 PM

Latest Trade Ideas articles

Today 07:49 AM

Today 04:24 AM

Yesterday 10:48 PM