Asian Indices:

- Australia's ASX 200 index rose by 54.1 points (0.8%) to close at 6,827.10

- Japan's Nikkei 225 index has risen by 31.67 points (0.1%) and currently trades at 29,747.54

- Hong Kong's Hang Seng index has risen by 160.78 points (0.56%) and currently trades at 28,994.54

UK and Europe:

- UK's FTSE 100 futures are currently up 31 points (0.46%), the cash market is currently estimated to open at 6,780.70

- Euro STOXX 50 futures are currently up 9 points (0.24%), the cash market is currently estimated to open at 3,838.84

- Germany's DAX futures are currently up 31 points (0.21%), the cash market is currently estimated to open at 14,492.42

Monday US Close:

- The Dow Jones Industrial rose 174.82 points (0.53%) to close at 32,953.46

- The S&P 500 index rose 25.6 points (0.65%) to close at 3,968.94

- The Nasdaq 100 index rose 145.25 points (1.12%) to close at 13,082.54

Indices: European bourses wobble at their highs on vaccine halt

European shares were lower yesterday as Germany halted their use of the AstraZeneca vaccines, on reports it caused blood clots in some patients. The DAX printed a bearish outside candle, although with sentiment remaining buoyant and futures ticking higher, perhaps it can remain above its 10-day eMA. Still, having closed to a record high recently after breaking out of a multi-week resistance level, we’d be happy to see the DAX retrace towards 14,200 support – as this level could tempt bulls to return to the table.

The CAC could also do with a retracement as it appears overextended above its 10-day eMA. And yesterday’s bearish outside day above 6,000 suggests it could be ready. But as with the DAX, the trends still point higher from here.

As for the FTSE 100, price action remains choppy as ever. Yesterday’s Doji with a longer upper wick kissed 6,800 momentarily before falling back below the days’ open. With such fickle price action on the daily chart, it perhaps is better suited to intraday traders, if it must be traded at all.

RBA minutes reiterate dovish stance (in long form text)

The Reserve Bank of Australia (RBA) released the minutes of their March cash rate meeting. They reiterated that negative interest rates are “extraordinarily unlikely” and that rising bond yields can be attributed to optimism of the economic recovery. They will ignore transitory spikes in inflation and do not expect to hit their employment and inflation targets until 2024 at the earliest. With that said, RBA aren’t exactly known for moving first with policy these days and their outlook generally mirrors the Fed. So it will be interesting to see if the RBA take a more ambitious tone if or when the Fed upgrade their own outlooks.

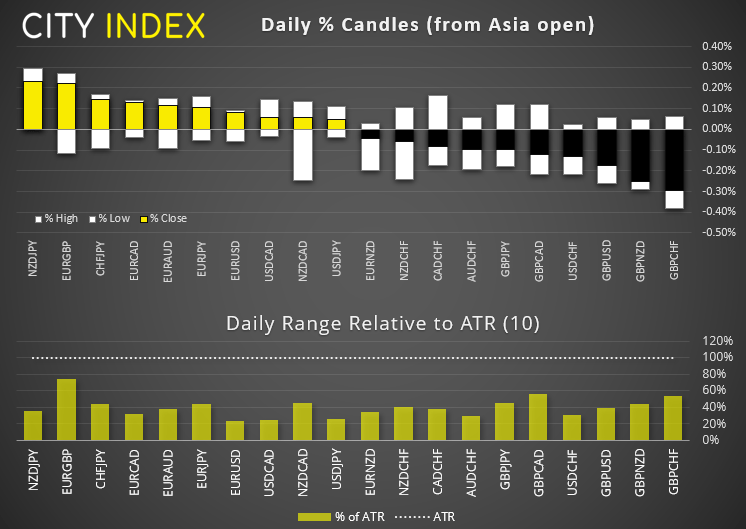

Forex: Tight range (again)

The US dollar was little changed overnight, although trades slightly lower and in the top half of Monday’s bullish range. The British pound was the weakest major overnight and the euro was the strongest, yet ranges were small again ahead of Wednesday’s FOMC meeting. Most forex majors and crosses we track remained below 50% of their 10-day ATR’s (average true ranges).

- USD/CAD produced a Riskshaw man Doji daily candle which teased, yet failed to close beneath, a multi-month low. This could leave USD/CAD to a bounce if US retail sales come in stronger than expected later today.

- USD/JPY remains defiantly bullish overall, although it etched out a minor within a potential supply zone beneath the June 2020 highs. A weak US retail sales print could take the wind out of its sales, although this pair has burned many bearish fingers on its way up to current levels.

- The pound was weaker across the board overnight and lost the most ground to the Swiss franc, making GBP/CHF today’s weakest pair. However, a retracement for GBP/CHF is not exactly overdue, having rallied over 11% since December’s low and stopping just shy of the 1.3000 barrier.

- EUR/GBP has poked its way to six day high as its correction from the 0.8537 low continues. Yet like most pairs the move lacks ambition in a low-volatility environment.

- GBP/USD has moved towards yesterday’s low. We may find this could be a frustrating pair to trade over the next 24 hours as we have the Fed and BOE meetings to contend with over Wednesday and Thursday.

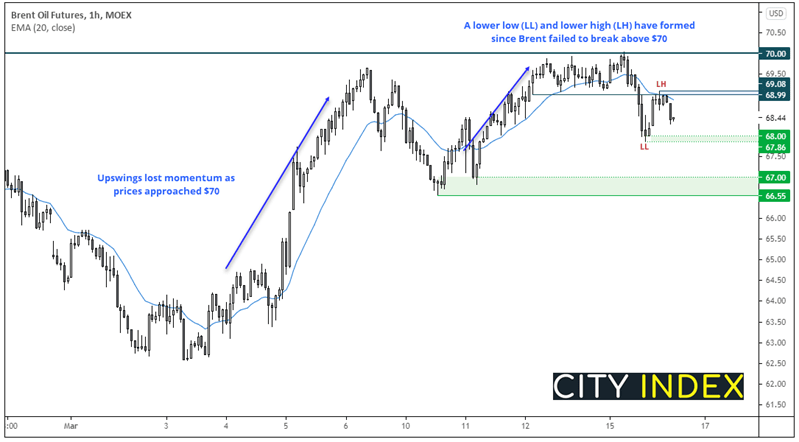

Brent: Time to correct?

The gains for oil markets this year have not gone unnoticed. Fundamentals and the technical landscape have aligned for a great run for Brent to hit $70, but perhaps now it is time for a good old fashioned retracement. Take note that we are not calling for Armageddon type bear-market type, but a simple movement against its trend.

One observation from the daily chart (not pictured) is that volatility has increased leading into the highs of $70. This shows the dynamic of the trend has changed and could perhaps be signs of distribution at the highs (before it really does turn lower).

We saw a small bearish pinbar on Friday followed by a bearish engulfing candle yesterday which rolled over after touching $70. So we are now looking to position ourselves on an intraday timeframe as we anticipate further weakness.

Switching to the four-hour chart shows a prominent lower low and lower high have formed below $70. After retracing to around $69, bearish momentum has returned overnight to show supply at this key level.

- Bears can consider fading into (shorting) into minor rallies below the 69 highs

- The lows between 67.86 and 68.00 are the interim target (yesterday’s low)

- A break beneath 67.86 brings the 66.55 – 67.00 lows into focus

- A break above 69.08 invalidates the near-term bearish bias

Elsewhere in commodities:

WTI trades around $64.50 after falling to $64 yesterday. Yesterday’s volatile Doji suggests WTI requires caution, as the intraday price action appears to be more ambiguous than brent’s.

Gold prices are testing yesterday’s highs around 1734.50, but we’d like to see a break above 1740 resistance sooner than later, otherwise we risk another cycle lower. And this is perfectly plausible given the tight ranges seen for the dollar. Still, a break above 1740 brings our 1760 bullish target into clear view.

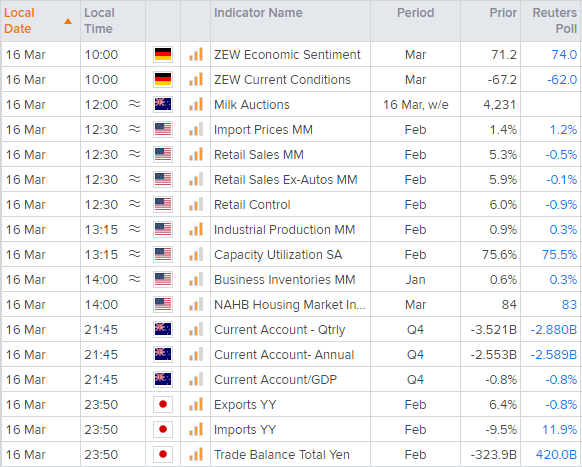

Up Next (Times in GMT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Germany’s ZEW economic index is the main calendar event in the European session. It beat expectations in February due to high expectations for a retail spending spree that never materialised (retail sales fell -0.45% in January and -8.7% YoY). Sentiment was already lower for European equities yesterday due to reports of Germany (among others) halting the AstraZeneca vaccine, so we suspect euro forex pairs and bourses may be sensitive to a weak print today, if that materialises.

Retail sales in the US are expected to rise 5.3% and feed further into the economic rebound / higher inflation narrative, even if they fall slightly short of expectations. We’d therefor expect that narrative to become amplified if retail sales beats the consensus, and provide further support the Down Jones, S&P 500 and Russell 2000, which are already at record highs.

Latest market news

Latest Indices articles

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM