US futures

Dow futures -0.12% at 31813

S&P futures -0.76% at 3830

Nasdaq futures -1.63% at 11400

In Europe

FTSE -0.6% at 6970

Dax -1.2% at 13082

Learn more about trading indices

Meta earnings due after the close

After three days of solid gains, stocks are wobbling, with the tech-heavy Nasdaq set to lead the charge lower.

The fall comes after stocks had rallied hard across recent sessions after a slew of weaker-than-forecast data, including home sales and consumer confidence, prompted speculation that the US economy is cooling and that the Federal Reserve could slow the pace at which it is hiking rates after the November meeting.

According to the CME FedWatch tool, the market is now pricing in a greater probability of a 50-basis point hike than a 75-basis point hike in December now.

The economic calendar is relatively quiet, with housing data in focus. US mortgage rates rose to 7.16% its highest level since 2001.

Today disappointing results from Alphabet and Microsoft have unnerved investors at the start of big tech earnings. Ad revenue growth has been a worry since Snap’s earnings last week, and Alphabet’s results have confirmed that no company is immune for the slowdown in digital ad revenue.

Corporate news:

Alphabet is falling pre-market after disappointing earnings. Google’s parent company was disappointed on both earnings and revenue. EPS was $1.06 vs $1.25, expected on revenue of $69.09 billion against $70.58 billion forecast. Ad revenue was $54.48 billion, below expectations of $56.98 billion, sending shivers across the sector. The slowdown in ad spending is likely to be a key theme across social media stocks. Alphabet trades 6% lower ahead of the open

Microsoft beat earnings and revenue expectations but trades 5% lower pre-market after cloud revenue disappointed and quarterly guidance disappointed. Microsoft reported EPS of $2.35 vs $2.30 forecast, on revenue of $50.12 billion vs $49.61 billion. Concerning guidance, Microsoft forecast $52.35 -$53.35 billion in revenue in fiscal Q2, below the $56.05 billion analysts expected.

Meta is due to report after the close and is expected to show ongoing struggles owing to the tough macroeconomic climate, growing competition from Tik Tok and fallout from Apple’s ad-tracker.

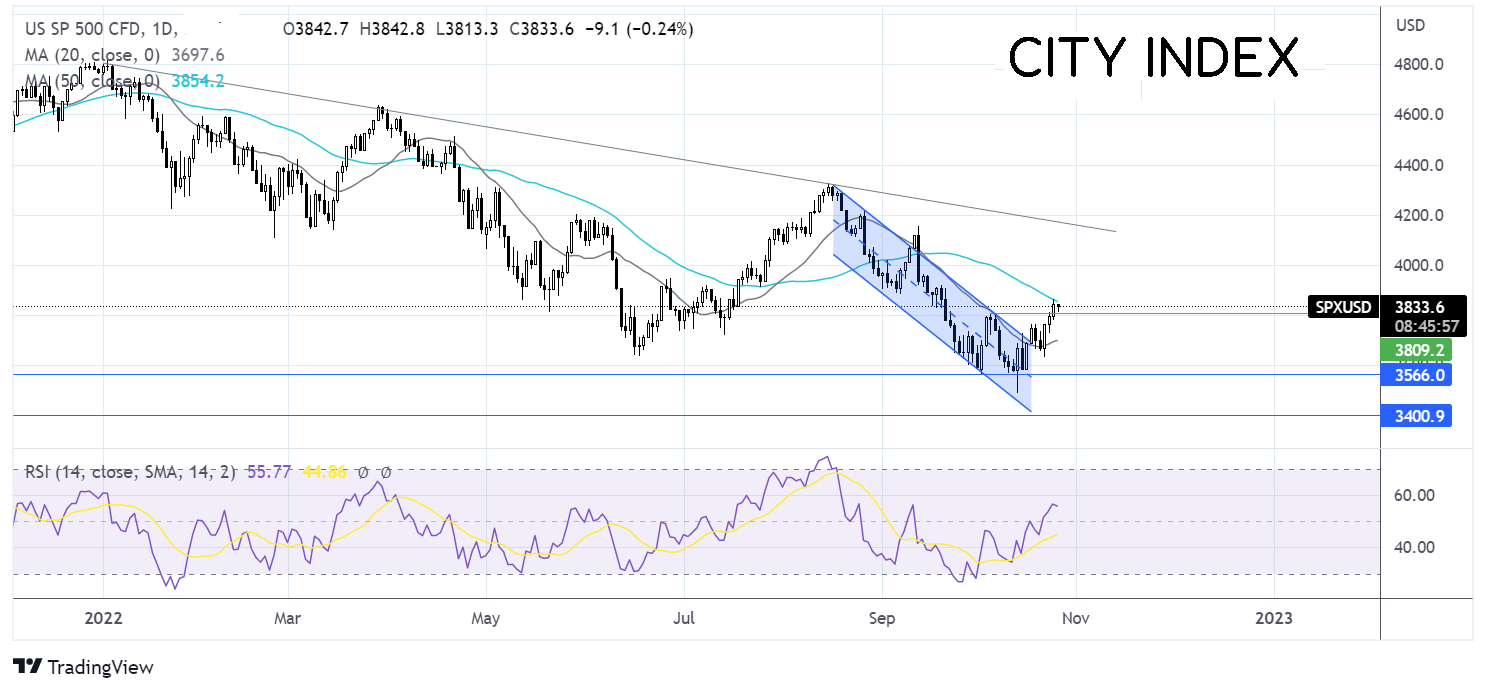

Where next for the S&P500?

The S&P has extended its recovery from the 2022 low, out of the multi-week falling channel and above the 20 sma, but has stalled at the 50 sma above 3800. The RSI above 50 keeps buyers hopeful of further upside. Buyers need to push over the 50 sma at 3860, before brining 3900 round number into play. Should sellers successfully defend 3800, the price could fall to 369 the 20 sma, before re-entering the falling channel.

FX markets – USD falls, GBP rises

The USD is falling for a fifth straight session as bets are rising that the Federal Reserve will slow the pace at which it hikes rates after the November meeting. The US dollar index trades at a level last seen three weeks ago.

AUD/USD is outperforming its peers after Australian inflation was hotter than expected in Q3, rising 7.3% annualized, up from 6% in Q2 and well ahead of the 7% forecast. The data supports a more aggressive approach from the RBA, just as the Fed looks like it may start slowing rate hikes.

GBPUSD is extending its gains after jumping 1.2% yesterday and trades at a 3 week high.. Optimism that Rishi Sunak and his team will restore stability and credibility in the UK is overshadowing the very difficult economic situation that he has inherited.

GBP/USD +0.8% at 1.1560

AUD/USD +1.4% at 0.6476

Oil steady as oil inventories rise

Oil prices are holding steady on Wednesday as higher-than-expected inventories are offset by supply concerns.

Data yesterday showed that oil stockpiles rose by 4.5 million barrels in the week ending October 21, according to the latest API data. This was ahead of expectations, as forecasts had been for a build of 200,000 barrels.

The higher-than-forecast stockpiles reinforced concerns that a global recession would weigh on demand.

Meanwhile, these concerns were being offset by OPEC+ production cuts which will come into force as from November.

Looking ahead EIA stockpile data is due later.

WTI crude trades +0.8% at $86.90

Brent trades +0.73% at $9256.

Learn more about trading oil here.

Looking ahead

15:00 BoC

15:00 US New Home Sales

15:30 EIA crude oil